Making Tax Digital for Income Tax

HMRC has at last published regulations for the record-keeping requirements for Making Tax Digital for Income Tax Self Assessment. What’s the full story?

Starting in 2023/24, if you receive income greater than £10,000 per year from self-employment or rental income from land or buildings you’ll be required to make quarterly online reports of your business/rental income and outgoings, plus an annual summary.

The first MTD ITSA report will therefore be for the quarter ended 5 July 2024, however you must have digital record keeping systems in place earlier.

The update information that must be provided in a quarterly update is dependent on the relevant person’s business or businesses.

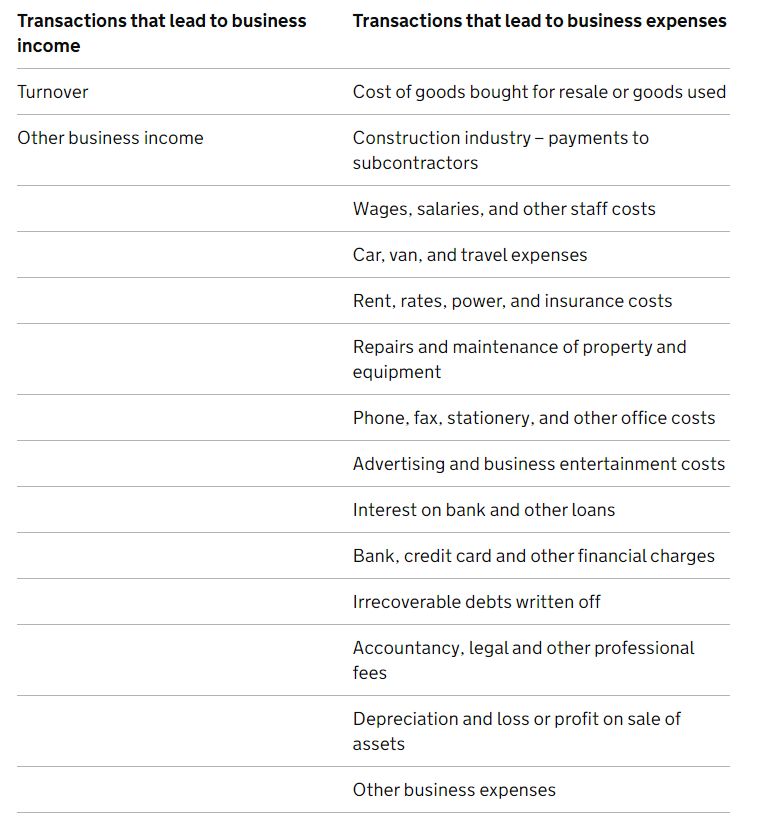

Businesses with trade profits:

A relevant person with trading income must provide the following update information in each quarterly update:

- quarterly period start date

- quarterly period end date

- totals of the amounts falling within the categories of transactions set out in the following table:

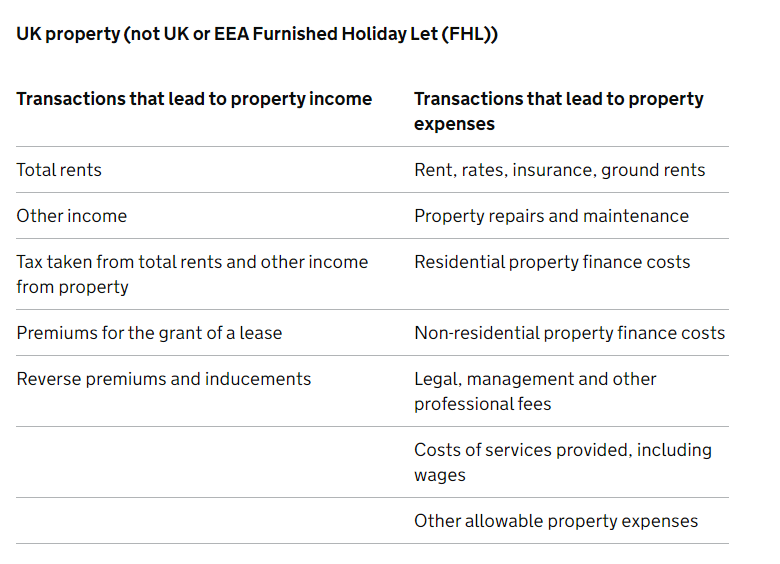

Businesses with property income:

A relevant person with property income must provide the following update information in each quarterly update:

- quarterly period start date

- quarterly period end date

- totals of the amounts falling within the categories of transactions set out in the following table:

Software. MTD ITSA means you’ll either have to use HMRC-approved software to keep your day-to-day business/rental income and expenses records or use a spreadsheet plus so-called bridging software to collate the data and make MTD reports to HMRC. HMRC’s draft regulations published on 1 July 2022 set out the format and type of information required.

Your reports must summarise income and outgoings from your records into the categories currently used for your annual self-assessment tax return. One difference is that you won’t be required to make adjustments for non-tax deductible items on the quarterly reports.

These will be required on the annual summary report only. Retail businesses will be able to make a special election to exclude certain information from their reports, such as erroneously recorded sales.

Tip. Reporting will be more straightforward if you choose to use HMRC- approved software as the income and expenses categories will already be set up. If you use bridging software you’ll need to digitally link your records to fit the software.

For more information…